Data tokens on this page

Financial Solutions

Financial Solutions

Estate Planning Tax Strategies

Procrastination can be the biggest enemy of sound estate planning—but as Benjamin Franklin so astutely noted over 200 years ago, “In this world nothing can be said to be certain, except death and taxes.”

While a proper estate plan will not enable you to avoid death, it can help eliminate, or at the very least, minimize estate taxes.

Federal estate taxes are imposed when an individual’s taxable estate exceeds the “applicable exclusion” amount. For 2022 that amount is $12,060,000. If you are concerned that you may have a taxable estate, there are a variety of trust and gifting strategies available that may help reduce or even eliminate your tax bill.

Determining the most appropriate estate planning strategies requires careful consideration by you, your Trust Administrator, and your other financial and legal advisors. The following is a sampling of some strategies to get you thinking about how you can better position your estate.

Strategies

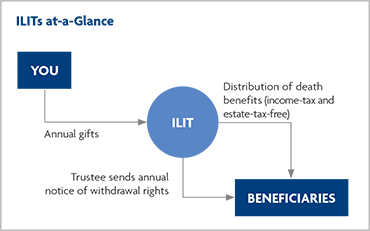

Irrevocable Life Insurance Trust (ILIT)

An ILIT can be an effective strategy for transferring wealth to your beneficiaries without incurring any income tax or estate

tax liability. An ILIT is designed so that death benefits remain outside of your taxable estate.

You make annual exclusion gifts—up to $16,000 per beneficiary in 2022—to an irrevocable trust. You must then notify the beneficiaries of their right to withdraw the

gift for a limited amount of time. This temporary right to withdraw creates a “present interest” in the gift and allows the ILIT to qualify for the annual gift tax exclusion.

An independent trustee then uses these gifts to acquire and maintain life insurance on you. Because the ILIT is the insurance policy’s owner, the death benefits are not considered part of your taxable estate. At the time of the ILIT’s creation you have control over how and to whom the death benefits are to be distributed, i.e. immediately distribute proceeds out to beneficiaries, keep proceeds in the ILIT and have the trustee pay income and principal to beneficiaries according to standards you set, or use proceeds to cover estate taxes.

Portability Election

The portability election is an estate tax-saving strategy that is used to “transfer” a deceased spouse’s applicable exclusion to the surviving spouse ($12,060,000 in 2022). This approach depends on action taken after one spouse dies. You must rely on the executor of your estate to make important tax decisions after your death, and be willing to incur the extra costs necessary to file a timely and complete tax return—due nine months after death.1

It is important to note that state exclusions are not portable, and therefore, this is not an optimal choice if you live in a state that imposes its own estate tax. Additionally, portability does not address asset appreciation. Any appreciation on the deceased spouse’s assets will be included in the estate of the surviving spouse. Moreover, portability does not apply to the GST tax exemption; any unused portion does not transfer to the surviving spouse. In many cases, a credit shelter trust (discussed below) will continue to be the preferred approach for married couples who want to use both of their applicable exclusions.

Credit Shelter Trust

Unlike the portability election, which is made after the death of one spouse, a credit shelter trust must be created before death (within the terms of couple’s revocable living trusts). The credit shelter trust has many different names: “bypass” trust, “B” trust in an “A-B” trust plan, or “family” trust in a “family/marital” trust plan. It enables married couples to use each spouse’s applicable exclusion.

As previously noted, federal estate taxes are imposed when an individual’s taxable estate exceeds the applicable exclusion amount. However, married couples do not automatically get the benefit of two exclusions. A married couple can avoid federal estate tax on estates worth up to twice the applicable exclusion ($24,120,000) by implementing a credit shelter trust.

The trust is created from the estate of the first spouse to die; an amount equal to the applicable exclusion is set aside in the trust. The surviving spouse can receive income from the trust and may have access to principal. When he or she dies, trust assets are distributed to heirs as directed in the trust document. Because the surviving spouse has limited control over trust asset distribution, they are not considered part of the taxable estate. Using this strategy is important because, at the flat estate tax rate of 40%, being able to protect an additional $12,060,000 could translate into significant estate tax savings.

Gifting

You may gift up to the annual exclusion amount ($16,000, if single and $32,000, if married for 2022) to as many individuals as you wish without incurring gift taxes. For example, a married couple with two married children and four grandchildren can give $32,000 to each child, their spouse, and each grandchild—a total of $256,000 free from gift taxes. Gifting also removes any future growth of the gifted assets from your estate. There are many gifting vehicles available to help reduce and transfer wealth out of your taxable estate. Some of these include:

Front-loading a 529 college savings plan allows you to make five years’ worth of annual exclusion gifts at one time without incurring any gift tax liability. If, however, you should die within five years of the gift, the pro-rated portion for the years after death will be included in your estate for estate tax purposes.

Direct tuition or medical care provider payments for your loved ones’ educational or medical costs are not considered part of your annual or lifetime gift tax exemption.

Grantor retained annuity trusts (GRAT) are useful in a low-interest-rate environment and also work especially well with assets currently depressed in value. You (the grantor) transfer assets to a trust for a specified term, during which time you receive an annuity from the trust. The annuity payments reduce the gift’s value for gift tax purposes. At the end of the term, the remaining assets pass to the beneficiary. If, however, the grantor dies before the specified term ends, the assets are included in the taxable estate.

Charitable remainder trusts (CRT) can help reduce your overall gross estate, create a higher cash flow during your lifetime while generating an income tax deduction, lower investment risk, and provide greater portfolio diversification. CRTs are good for highly appreciated stock, and for those who are charitably inclined. A charity you choose is given a vested future interest in property—you retain an income for life with the remainder interest going to the charity.

Charitable lead trusts (CLT) are used when income is not needed. Instead of contributing a remainder interest, the grantor donates an asset’s income interest for a period of years to a charity with the remainder interest then passing to a beneficiary. The grantor or grantor’s estate receives an income tax deduction for the value of the interest income. CLTs are often designed to take effect at the grantor’s death, thus reducing the gross estate.

Getting Started

Wintrust Wealth Management offers a comprehensive suite of trust and estate planning solutions through its trust affiliate, Wintrust Private Trust Company, N.A. Contact your Wintrust Wealth Management professional to learn more.

1. Revenue Procedure 2014-18, issued on January 27, 2014, will allow taxpayers who meet certain criteria to obtain an extension of time to make a portability election simply by filing an estate tax return in accordance with the procedure the IRS has set forth.

This information may answer some questions, but is not intended to be a comprehensive analysis of the topic. In addition such information should not be relied upon as the only source of information, competent tax and legal advice should always be obtained.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.