Data tokens on this page

Financial Solutions

Financial Solutions

An Introduction to Donor-Advised Funds

A donor-advised fund can be an efficient, simple, and flexible way to give to charity while enjoying the tax benefits and avoiding the cost and administrative burden often associated with private foundations.

With the case for charitable giving stronger than ever, many donors are grappling with the highly-personal decision of how to best conduct their planned giving. Should you contribute directly to charities, create a donor-advised fund (DAF), or donate to an existing one? Each donor’s situation is different, so it is important to discuss your charitable giving goals with a financial professional. Our trust and investment professionals are often able to help our clients have a greater impact than if they were making decisions on their own.

What is a Donor-Advised Fund?

A donor-advised fund is a charitable giving vehicle administered by a third party and created for the purpose of managing charitable donations on behalf of an organization, family, or individual. A donor-advised fund offers the opportunity to create an easy-to-establish, low cost, flexible vehicle for charitable giving as an alternative to direct giving or creating a private foundation. Donors enjoy administrative convenience, cost savings, and tax advantages by conducting their grant making through the fund. These types of funds are the fastest growing charitable giving vehicle in the United States, with more than 700,000 donor-advised funds established, holding over $121 billion in assets.

Because the fund is housed in a public charity, donors receive the maximum tax deduction available, while avoiding excise taxes and other restrictions imposed on private foundations. Further, donors do not incur the cost of establishing and administering a private foundation, including staffing and legal fees. In order to ensure the maximum charitable deduction, it is necessary for the third-party Foundation to own and control the funds contributed.

The donor can advise the Foundation as to the disposition of the funds. As such, they are not legally bound to the donor, but make grants to other public charities upon the donor’s recommendation. Most foundations that offer donor-advised funds will only make grants from these funds to other public charities, and will usually perform due diligence to verify the grantee’s tax-exempt status.

Tax Benefits of a Donor-Advised Fund

Giving with a donor-advised fund can be a tax-efficient way to conduct your philanthropy. Below are a few strategies to reduce your tax liability using a donor-advised fund while increasing your charitable impact.

- Grow Your Charitable Dollars Tax-Free: The charitable dollars in your donor-advised fund can be invested before they are granted out. With market growth, your DAF balance can also grow, potentially increasing funds available to grant. Moreover, while you can take an immediate tax deduction for the gifts you make to your DAF, you will not be taxed on any growth, since the assets belong to the DAF’s charitable sponsor.

- Reduce Tax Burden in a Windfall Year: DAFs can reduce tax burdens after a windfall situation, such as receiving an inheritance, selling a business, or experiencing strong market returns. You can take an immediate tax deduction when you make a charitable contribution to your DAF, reducing your tax liability. DAFs allow you to recommend grants to your favorite charities over time, so you can effectively pre-fund years of giving with assets from a single high-income event.

- Reduce or Eliminate Capital Gains: Direct donation of publicly traded securities (or other illiquid gifts) is one of the most common ways to fund a DAF. This is a particularly tax-efficient method because securities held for more than one year can be donated at fair market value, and are thereby not subject to capital gains tax. If a donor liquidates their assets and later donates the proceeds to their DAF, the amount would be reduced by capital gains tax, leaving less available for philanthropy. Donors receive an immediate tax deduction of up to 30% of adjusted gross income (AGI) for gifts of appreciated securities, mutual funds, real estate, and other assets, and can enjoy five-year carry-forward deduction on gifts that exceed AGI limits.

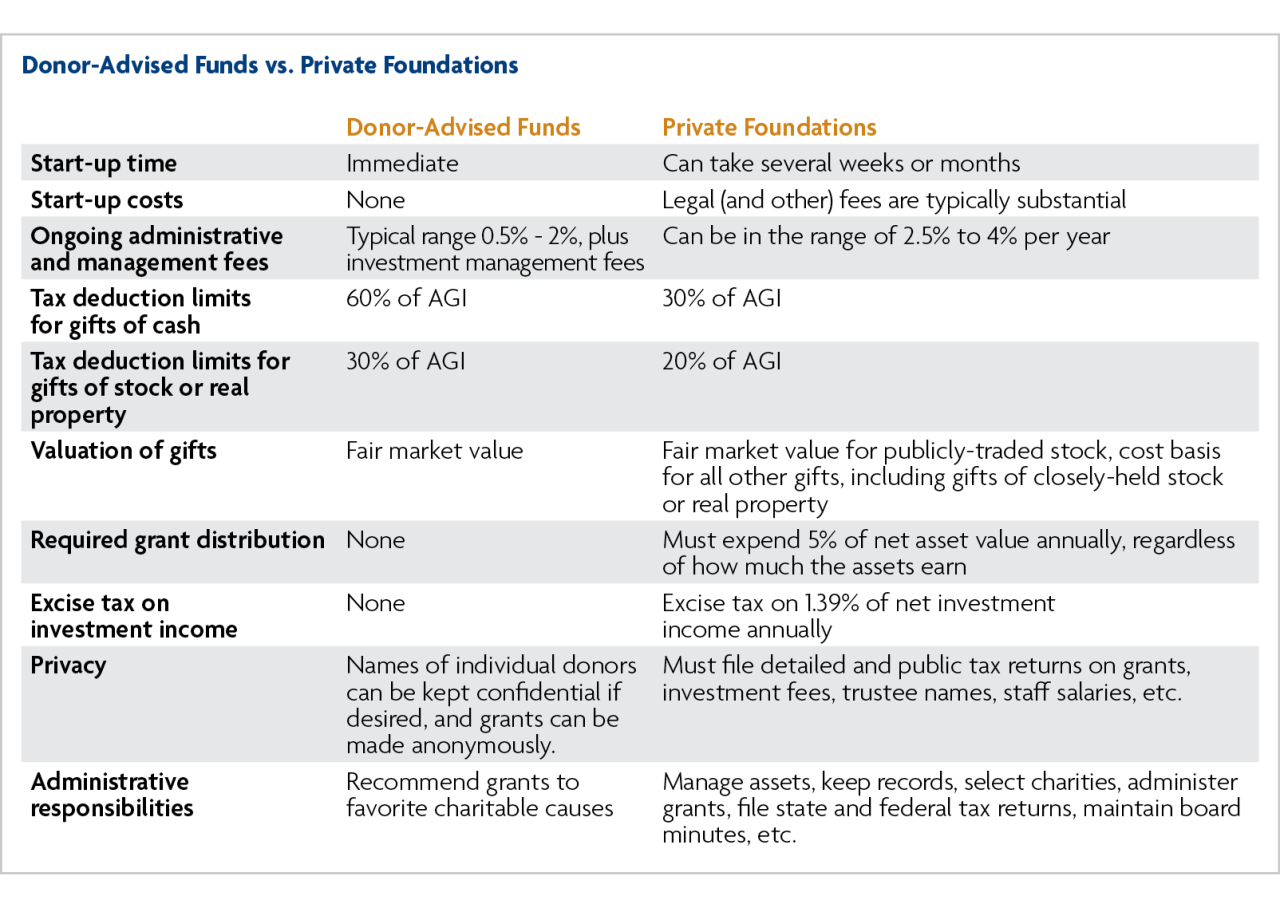

Comparison to a Private Foundation

A donor-advised fund is often compared to a private foundation, another vehicle for making lifetime grants to charity. A private foundation is formed by a family or an individual who must then apply for tax-exempt status with the IRS. A donor-advised fund can be established by completing a simple Donor Application and Agreement. Contributions to a private foundation are deductible up to 30% of a donor’s adjusted gross income (AGI) for cash and 20% AGI for appreciated securities. A contribution to a donor-advised fund is a contribution to a public charity; therefore, the deduction limitations are higher. A donor may take a deduction for the full fair market value of his or her gift up to 50% AGI for cash and 30% AGI for appreciated securities. A summary of the differences is shown in the table below.

What to Donate

Donor-advised funds accept both cash and securities; which is most beneficial for you to contribute depends on your particular situation. A donation of cash is immediately deductible, as noted earlier, up to 50% of your adjusted gross income (AGI). A donation of securities is also deductible immediately, but only up to 30% of your AGI. However, if you have highly appreciated securities, there is an additional benefit of donating them. You can obtain a deduction, up to 30% of AGI, for the full fair market value of the securities at the time of the donation. This means that you pay no capital gains tax and still receive a deduction equal to the full fair market value of the securities donated, making a donation of appreciated securities particularly valuable. Remember that your donation will be based upon the market value on the day of your donation, not the price for which the securities may ultimately be sold. Also, any deduction amount which exceeds the percentage limitation of 50% or 30% AGI in the year of the donation can be carried forward for five years. Finally, you should consult your tax advisor when deciding whether a donor-advised fund is right for you, and which type of asset is most beneficial for you to contribute.

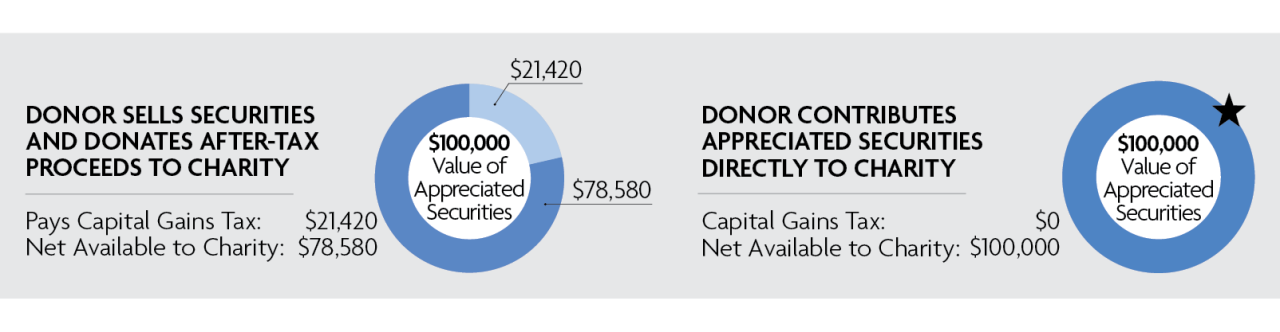

Donating Appreciated Stock: An Example

By donating appreciated stock held for more than one year directly to a DAF—rather than liquidating it and then donating the proceeds—philanthropists can reduce their tax liability by eliminating capital gains tax, as well as reducing their marginal income tax.

In the hypothetical example below, a donor has $100,000 in long-term appreciated stock, and its original cost-basis purchase price was $10,000. Using a DAF, this donor would have more available to give to charity and would pay less in taxes. This strategy can often allow donors to give more than 20% more to the causes they care about.

Note: For the purposes of illustration, this hypothetical example assumes that all realized gains are subject to the federal long-term capital gains rate of 20% and the Medicare surtax of 3.8%. No other state taxes are taken into account.

A Legacy of Gifting

Many people want to pass the habit of giving onto their children and involve the entire family in the grant making process. This is often cited as a significant reason for creating a private family foundation. However, you can establish the same family legacy with a donor-advised fund. At the time you establish your fund, you can name more than one Donor Advisor and you can name Successor Donor Advisors to act when you are no longer able to do so. Furthermore, you can name your fund as you would a private foundation. For example, you might entitle your fund “The Jones Family Charitable Giving Fund” and name yourself and your spouse as initial Donor Advisors and your children as Successor Donor Advisors, thereby involving them in the grant-making decisions as soon as they are old enough. As an alternative, if you want your children to be directly involved with you in making grant decisions, you can name them as additional Donor Advisors. The giving can continue after your death for another generation, after which the balance in your fund will be gifted to a charity or particular area of interest, which you can specify at the time you establish the fund or thereafter.

Getting Started

The Trust Administrators at Wintrust Wealth Management can work closely with you to craft an effective and meaningful giving strategy. Contact us to discuss your options.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.