Data tokens on this page

Financial Solutions

Financial Solutions

A Guide to Wiser Giving

There are many complex vehicles through which to give and understanding the tax advantages associated with them will help you give more wisely and help expand your giving power.

We are a generous nation. Just last year, over 150 million Americans made a total of $449 billion in charitable contributions—the highest amount on record and 5.1% more than in the prior year.1 Whether your goal is to give to charity, bequeath your estate to heirs, or both, doing so without a well-considered plan can significantly limit the reach and impact of your efforts.

Whether you plan to give hundreds, thousands, or millions, the support of a financial professional and a basic understanding of the estate, gift, and income tax implications of gifts to charity and family are needed to navigate the gifting terrain. This, coupled with a clearly defined giving plan, will enable you to maximize the impact your gifts have on the world, your community, and your family

Create a Giving Plan

Before you can begin to maximize the effect of your generosity, you must decide what you hope to accomplish. Begin by determining how you wish to divide your gifts between family and charity. For family, consider how you would prefer to give during your lifetime to support education, housing, medical and living expenses, and how much you wish to bequeath and to whom. For charitable giving decisions, the options often become more varied and challenging. To begin, consider the following:

- Matters of Interest: What issues and causes are most important to you and where would you really like to make a difference? Would you like your impact to be felt at the individual, organizational, community, or policy level?

- Geographic Focus: Do you prefer to give to organizations serving local, state, national, or global needs?

- Level of Involvement: Do you wish to remain anonymous? If not, how would you like to be recognized for your gifts? How involved do you want to be in the life of the organization? Do you prefer to provide financial support, participate on boards, or have direct involvement in the day-to-day work of the organization?

Next, articulate these ideas in a giving mission statement. Typically one to three sentences, a giving mission statement denotes your giving goals and the methods that will be used to achieve them. It serves as a guidepost for your decision-making and a tool to help you assess your progress. It consists of the answers to three fundamental questions:

- What are the major areas you want to affect through your giving and why?

- What types of organizations do you seek to support in these areas?

- Are there specific methods or key criteria that will guide your giving?

Deciding where to give is the next step. There is no shortage of nonprofit organizations providing honorable services. Fortunately, they are all considered part of the public trust and must follow strict operating guidelines, which make them relatively easy to research, evaluate, and monitor. Guidestar.org is an excellent source of information on nonprofit organizations. Bear in mind that when selecting charities, it is critical to ensure they are qualified for tax purposes as 501(c)(3) entities by the IRS. You can check the status of a specific charity on the IRS website at apps.irs.gov/app/eos.

Finally, decide how best to give. There are many means for giving both to charity and to family. What follows is a description of the most common giving vehicles.

Means of Charitable Giving

Charitable solutions generally fall into two categories: Outright donations; and those that also provide income to the donor. Those providing income are known as split-interest vehicles and are often used as part of the retirement and estate planning process. The most broadly applicable of these vehicles are charitable gift annuities and charitable remainder trusts.

Charitable Gift Annuity

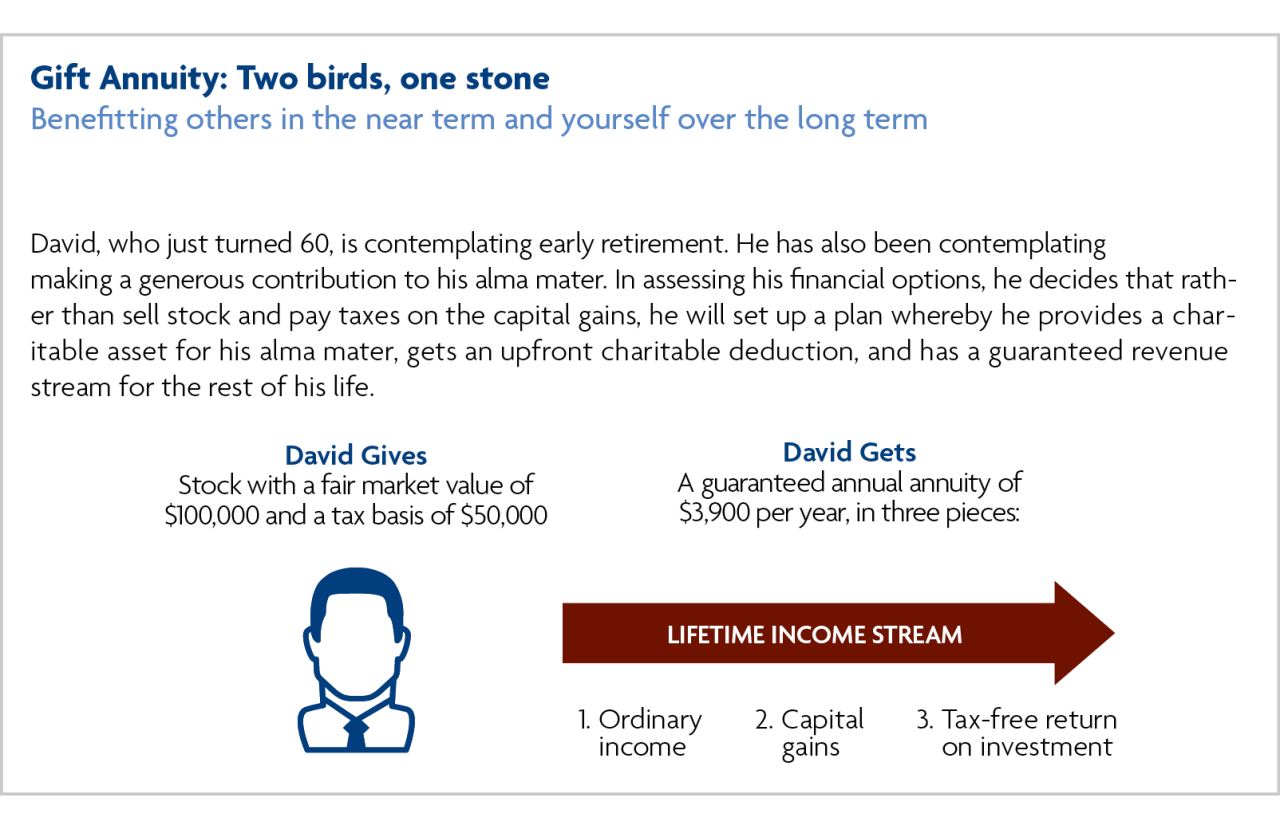

A charitable gift annuity is a contract between a donor and a charity under which the charity—in return for a transfer of cash, marketable securities, or other assets from you—agrees to pay a fixed amount of money to you and one more individual if you choose, for your lifetime(s). Such payments include the earnings on the reserve account and a part of the principal in the reserve account. The ratio of these parts, that is, the parts that are principal and earnings, depends upon your age(s).

The American Council on Gift Annuities (ACGA) publishes an annual schedule of gift annuity rates by age for single and joint annuities. The gift in the example on the following page is $100,000. Effective July 2020, the rate for a 60 year old is 3.9%, meaning an annual payout of $3,900.

The issuing institution guarantees the income, as it becomes a legal obligation of the charity. However, close attention to the credit worthiness of the charity is important as you will be reliant on the charity to provide income for the rest of your life. The benefits include a large charitable deduction in the year of the gift plus a lifetime stream of taxable income. The charitable deduction is equal to the net present value of funds estimated to remain for the charity at your death, as calculated by IRS formulas with an assumed factor for your longevity.

Generally, this vehicle works best if you want simplicity, desire fixed income payments, wish to benefit no more than one charity or other individual, and have cash, appreciated securities, or real estate to donate.

Charitable Remainder Trusts

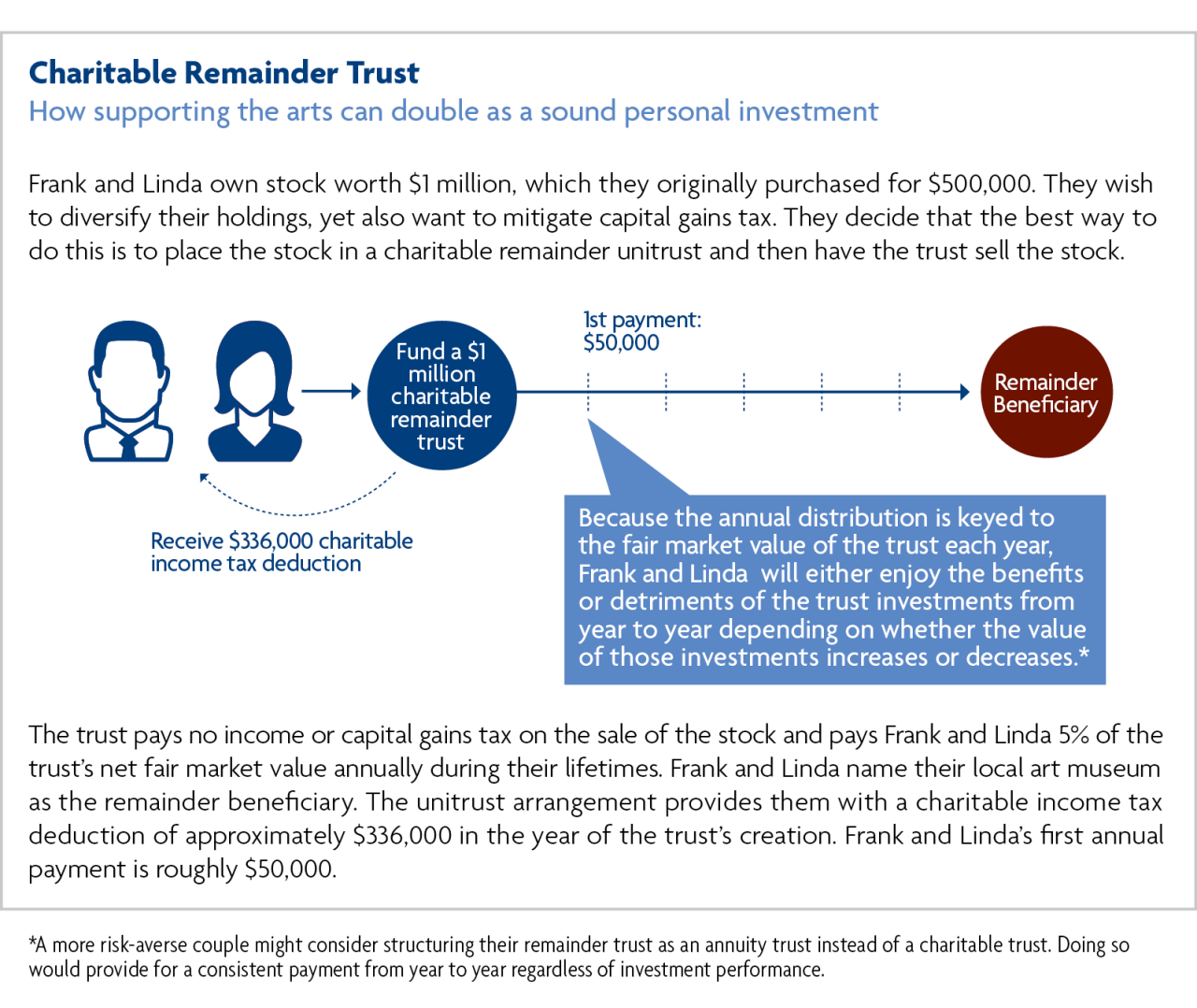

A charitable remainder trust (CRT) is an irrevocable trust that you would typically fund with highly appreciated assets. The CRT is structured so that there is a current beneficiary—either yourself or a named individual—and a remainder beneficiary, which is an IRS-qualified 501(c)(3) charity, such as a private foundation. The CRT makes annual distributions to you in either a fixed amount or as a percentage of the value of the trust. These are paid for a period of years that can either be for your life or for a set period you choose, not to exceed 20 years. The remaining value of the CRT is then distributed to the charity, as illustrated below.

The tax benefits of a CRT include a potential charitable deduction in the year of the transfer equal to the amount that will remain for charity, as estimated according to IRS prescribed calculations based on an assumed factor for your longevity. In addition, a CRT is exempt from tax on its investment income. Thus, a trustee of the CRT can sell appreciated assets and reinvest the full proceeds, allowing you to diversify from a concentrated position in a tax-efficient manner. If you choose to contribute to a CRT under your Will, an estate tax savings is produced, not subject to any percentage limitations, with the value of the remainder interest passing to the charity. Finally, a CRT can be an effective strategy for planning your retirement as the trust can provide income distributions that do not commence immediately. For example, the trustee can sell the appreciated assets, reinvest the proceeds, defer payment of tax and delay distribution to you until you reach age 65 and are, presumably, in a lower tax bracket.

If you do not mind delaying charitable gifting, desire an income stream, have cash, appreciated securities, or real estate to donate, and may want multiple income recipients, a CRT may be a good gifting option.

Donor-Advised Funds

As noted previously, there are additional ways to make donations that do not produce income for the donor. One of the most broadly used of these is a donor-advised fund.

A donor-advised fund is a program of a public charity that allows you to make irrevocable contributions to the charity, become eligible to take an immediate tax deduction for the full value of the contribution, and then make recommendations for distributing the funds to qualified nonprofit organizations. Donor-advised funds often can accept many types of assets, will allow you to name successors to continue family involvement, and afford you the right to remain anonymous.

As for tax considerations, you may be eligible to take a tax deduction of up to 30% of your adjusted gross income for contributions of securities, and up to 100% for cash contributions. You may also be able to eliminate capital gains tax for gifts of long-term appreciated securities.

A donor-advised fund can be a good giving vehicle if you want simplicity in grant making, are comfortable serving in only an advisory role, want higher charitable deduction income limitations, and wish to support multiple charities.

Community Foundations

A second commonly-used means of charitable giving that does not produce income for the donor is a community foundation. A community foundation is a permanent, nonprofit, charitable organization for public benefit. It is supported by local donors and governed by a board of private citizens who speak for the needs and well-being of the community. They accept many types of assets, offer multiple types of funds—frequently including donor-advised funds, and will often afford you the right to remain anonymous.

These foundations are organized to channel gifts from donors to a variety of charitable organizations in a local community. Individuals, families, businesses, and organizations create permanent charitable funds that help their region meet the challenges of changing times. The community foundation generally invests and administers these funds.

You can potentially take an immediate tax deduction—up to 100% of adjusted gross income for cash or 30% for appreciated assets—and may also be able to eliminate capital gains tax for gifts of long-term appreciated securities.

Means of Giving to Family

Often when people think of gifting, they think only of charities. However, an estate plan that incorporates giving to non-charitable beneficiaries, such as family members and other heirs, can help preserve assets and possibly reduce estate and gift taxes.

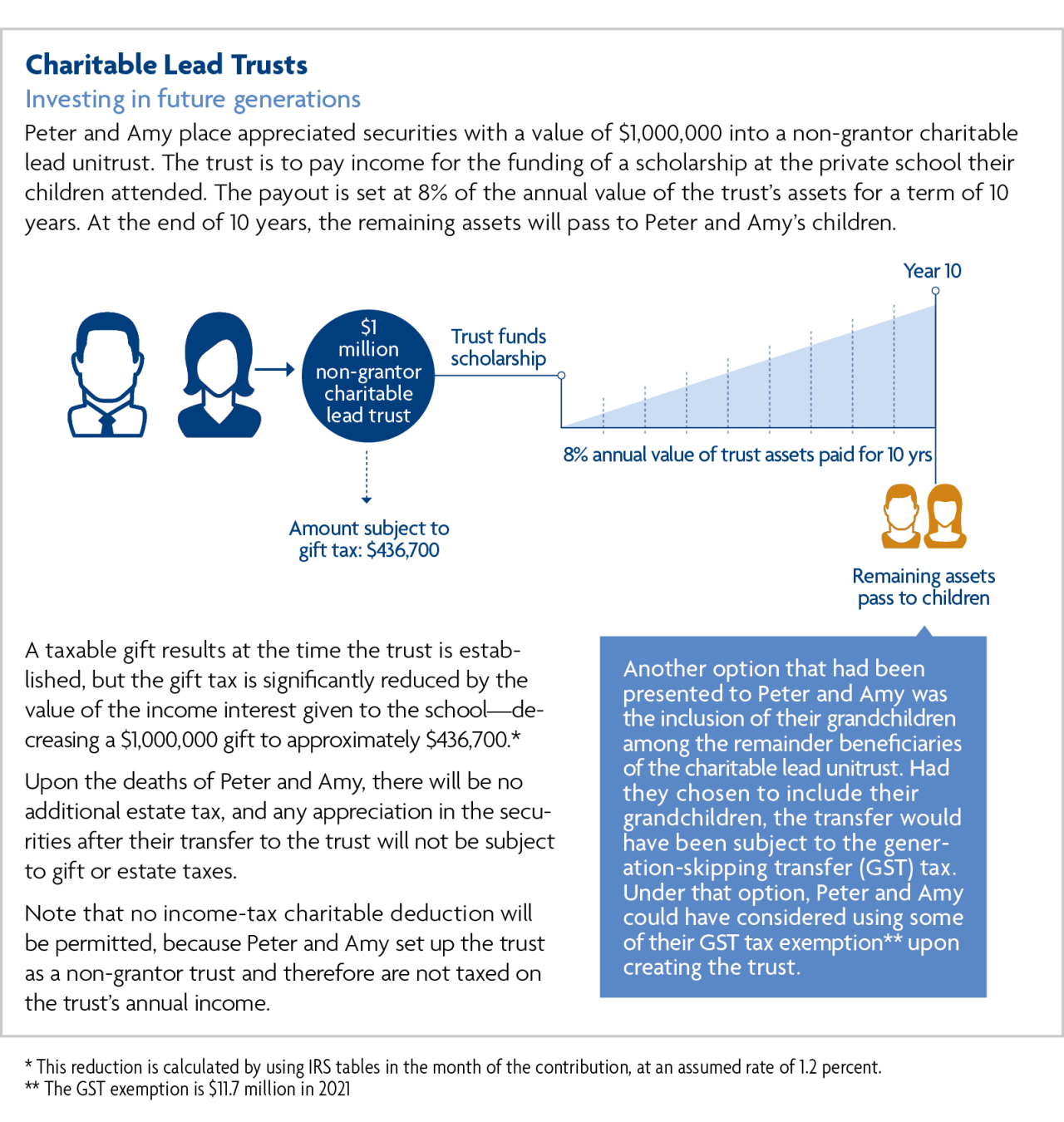

Charitable Lead Trusts

A charitable lead trust (CLT) is often thought of as the inverse of a charitable remainder trust. It is an irrevocable trust that provides a fixed amount or a percentage of the trust assets paid to a charity for a term of years or for the life of an individual or individuals. The remainder interest is either retained by the donor or given to a non-charitable beneficiary, usually a family member. A CLT is often created for lifetime giving and for estate planning purposes.

In many cases, the income-tax benefits of a CLT may not be as significant as the estate- and gift-tax benefits. For income-tax purposes, a CLT can be structured as a grantor trust, meaning the income earned by the trust is taxable to the grantor, or a non-grantor trust, meaning the income earned by the trust is taxable to the trust. For estate- and gift-tax purposes, there are other benefits of a CLT. If the contribution to the CLT is made during the donor’s lifetime, then the donor will also be eligible for a gift-tax deduction with the interest going to charity. If the remainder beneficiary is not the donor, then the donor could be subject to gift tax on the actuarial value of the remainder interest. The mechanics of a CLT are illustrated above.

Although there can be significant tax benefits to establishing a CLT, the donor should be aware of the potential implications of the generation-skipping transfer tax. If the remainder beneficiaries are or could be the donor’s grandchildren, when a distribution from the trust is made to these beneficiaries, the distribution will be subject to this tax unless the donor or the donor’s estate is able to allocate the donor’s generation-skipping tax exemption to the transfer or bequest. This tax can be significant.

The strategy works best for wealthy donors who anticipate having a taxable estate, already have ample cash flow for daily needs, have a keen interest in lifetime charitable giving, and wish to bequeath assets to heirs.

Gift Tax Exclusion Gifting

Each year, you may give any number of people up to $15,000 each (for 2021) in cash or assets—$30,000 if your spouse joins in making the gift—free of any gift tax. The recipient(s) is(are) also free of tax liability for such gifts. Gifts exceeding the annual gift tax exclusion are subject to a gift tax.

Note that current law allows you an unlimited exclusion for certain tuition and medical payments made on behalf of others. To qualify for this exclusion, you must make the payments directly to the educational institution or medical facility. Payments for medical insurance also qualify for the medical exclusion. However, payments for dormitory fees, books, supplies, and similar school expenses do not qualify for the tuition exclusion.

It is important to note that there is a lifetime gift tax exemption tied to the annual gift tax exclusion. The total amount you gift during your lifetime that is free of gift tax will be used to reduce the amount you can bequeath without being subject to estate taxes. For example, if you give away $3,000,000 during your lifetime, your federal estate tax exemption will be reduced to $8,700,000 (based on 2021 limits). In other words, $3,000,000 in lifetime gifts is subtracted from the 2021 federal estate tax exemption of $11,700,000, leaving only $8,700,000 of the exemption.

However, even if you have fully utilized your lifetime gift tax exemption equivalent amount, you are still able to take advantage of the annual gift tax exclusion amount. Conversely, the annual exclusion gifts do not reduce your lifetime gift exclusion. Furthermore, gifting to family members may provide additional tax benefits if taxable income can be shifted to family members with lower marginal tax rates than the donor.

Grandparent-Owned Life Insurance

If you are a grandparent, you can make sizeable gifts of cash using life insurance. Relatively small premiums can translate into large amounts of life insurance that can be earmarked for your grandchildren with the proceeds being distributed free of tax. Furthermore, grandparent-owned life insurance allows for you to place conditions on the gift and revoke the policy if such conditions are not met by the beneficiary, without penalty. Specifically, the policy may be cancelled with no surrender penalty after 10 years.

For example, consider a couple both age 70 and in good health. They purchase $250,000 of Survivorship Universal Life and name their grandchildren or a trust for the grandchildren as beneficiary. Assume the annual premium on the policy is $4,929 and both pass away at their joint life expectancy of 93. The resulting rate of return on the premiums paid producing the $250,000 proceeds in 23 years would be 6.13% tax-free.2

Special Options for Gifting To Minors

Transferring assets to minors can help to ensure that your children and grandchildren have the financial resources needed to go to college, buy their first home, start a business, or begin their own investment and estate planning. However, many people are uncomfortable giving large sums of cash or assets to their children or grandchildren outright. The following are a two of the main methods for gifting to minors:

UGMA/UTMA Accounts

Unified Gifts to Minors Act accounts or Uniform Transfers to Minors Act accounts provide that a custodian hold the property which can be used for the support, health, maintenance, and/or education of a child until attaining the age of majority—usually 18 or 21, depending on the state. At the age of majority, the child is entitled to the assets in the account.

UGMA and UTMA accounts are similar in many ways. Both are managed by custodians, and both allow parents, grandparents, relatives, and friends to make irrevocable transfers in any amount to the account. In addition, if you, acting as custodian, die before the funds are turned over to the child, the account may be taxable as part of the donor’s estate. The two account types differ in the type of assets you can transfer to them. UTMA law allows virtually any kind of asset, including real estate, to be transferred to a minor, whereas UGMA law limits gifts/transfers to bank deposits, securities (including mutual funds), and insurance policies.

For tax purposes, gifts made to UGMA and UTMA accounts are considered present interest gifts and are eligible for the annual gift tax exclusion. In addition, there is a minor income tax benefit in that the first $1,050 of the account’s unearned income (interest, dividends, or capital gains) is exempt from federal income tax if the child is under age 18 at the end of the tax year. The second $1,050 of unearned income is taxed at the child’s rate. Any unearned income over $2,100 is taxed at the higher of your or your child’s marginal tax rate.

529 College Savings Plans

Also known as Qualified State Tuition Programs, 529 plans are state-sponsored investment programs designed to help save for a child’s higher education. Each state develops its own program.

The Tax Cuts and Jobs Act of 2017 made significant changes to this vehicle. Now, 529 plans can fund educational expenses at any level, K-College. They can also fund private, public, religious schools K-12, and apprenticeships. Qualified expenses include tuition, fees, books, supplies, computers, and limited room and board.

There is a limit on withdrawals of $10,000 per year per child. Exceeding the limit invokes a 10% tax penalty in addition to taxes on investment growth.

You can front-load a 529 plan by gifting up to $75,000 ($150,000 if you gift-split with your spouse) in the first year, tax-free as long as the contribution is treated as a series of five equal annual gift tax exclusion gifts. If, however, you should die within five years of the gift, the pro-rated portion for the years after death will be included in your estate for estate tax purposes.

Additional Gifting Means

For very high net worth individuals and families with taxable estates, there are additional charitable vehicles to consider, including private foundations and supporting organizations. In addition, non-charitable vehicles such as irrevocable life insurance trusts (ILITs), grantor retained annuity trusts (GRATs), and intentionally defective grantor trusts (IDGTs) are some of the many other sophisticated gifting mechanisms for taxable or complex estates.

For more information on these options and means of fully leveraging them, contact a Wintrust Wealth Management professional.

Gifting Traps to Avoid

If you want to minimize or avoid taxes, your gifts must be properly structured. All your efforts may be for naught if you should fall into any of these common traps:

The kiddie tax rules: Beware of the kiddie tax rules when transferring income−producing property to children under age 18 or full-time students age 19-23. Unearned income above $2,200 is taxed at your marginal tax rate.

Gifts of retained interests or powers: Beware of making gifts of property in which you retain some financial interest (e.g., life estates, right of reversion, right of revocation) or powers (e.g., power of appointment). This property may be includable in your estate for estate tax purposes. For example, if you transfer ownership of your home to your child on the condition that you are allowed to live in the home for the rest of your life, then you have retained a financial interest in the home, which may be includable in your estate for estate tax purposes.

Delays in making a gift of life insurance: Do not delay in making a gift of a life insurance policy on your life. Transfers of policies on your life may be includable in your taxable estate if made within three years of your death.

Payments for tuition or medical care made to the donee: Do not make payments for tuition or medical care to the donee. You must make the payments directly to the educational institution or medical care provider in order to qualify the gift as tax exempt.

Overlooking gift-splitting: Do not forget the gift−splitting privilege for spouses who qualify, which can double the annual gift tax exclusion.

Overlooking the tax−exclusive nature of lifetime gift: Do not assume that lifetime gifts and transfers made at death result in the same tax effect. Remember that the tax−exclusive nature of lifetime gifts results in overall tax savings because the tax is removed from your estate.

Gifting in community property states: If you are married and live in a community property state (AZ, CA, ID, LA, NV, NM, TX, WA, or WI), gifts of community property you make to third persons may be limited by state law. For example, you may need the express or implied consent of your spouse, or you may be limited by the amount you can give each donee. The IRS may consider transfers made by your attorney−in−fact (agent or representative) to be revocable transfers. That means that those gifts may be includable in your estate for estate tax purposes. If you want your attorney−in−fact to make gifts on your behalf, make sure that you give express written authority in a power of attorney.

Closing

Clearly, the legal and tax landscape associated with giving—both charitably and to family—is complex and the options myriad. Tax-efficient charitable giving gets complicated quickly and the mechanics of charitable giving are worthy of careful planning attention. Furthermore, as changes in your life, your family, and your priorities materialize, your charitable giving plan should change as well. Beneficiary assignments should be reviewed on an annual basis to be sure they reflect the passing of loved ones, changes in marital status, and changes in your gifting priorities in accordance with your giving mission statement.

Your Financial Advisor can work closely with you and your legal and/or tax advisors to establish a sound charitable giving plan and help you make the most of your giving power.

1. Giving USA 2018 report, Giving USA Foundation; irs.gov SOI tax stats

2. Leaders Partners, Inc.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.