Data tokens on this page

A Primer on Long-Term Care Insurance

If you are concerned about the quality of life you will have as you age, it is important to explore what you can do now to maintain control over the type of care you receive in the future.

Without a long-term care strategy in place, your nest egg may be your only source of funds to pay for assisted-living expenses. If you would prefer to protect yourself from this potential expense and avoid the risk of becoming a burden to your loved-ones, you may want to consider long-term care (LTC) insurance.

Long-term care insurance is insurance coverage that offers protection for your nest egg against the high costs of extended health care if you become physically or mentally impaired. In exchange for your premium, most policies pay a fixed dollar amount for care you might receive at a nursing home, an assisted-living facility, or an adult day-care center, as well as your own home. LTC insurance minimizes disruption to your lifestyle and allows you to remain more independent. It provides flexibility by allowing you to select from a range of care options and benefits that enable you to get the services you need, where you need them.

Typically, to qualify for benefits you must be unable to perform two of the six activities of daily living (ADLs). These include, bathing, continence, dressing, eating, transferring (ability to move in and out of bed, a chair, or a wheelchair), and toileting. You may also qualify for benefits if you suffer from cognitive impairments, such as Alzheimer’s disease.

Although there is no guarantee that you will need long-term care, statistics indicate reasons you should think about it now; Someone turning age 65 today has almost a 70% chance of needing some LTC services at some point in their lives.1

Medicaid and Medicare Coverage

Medicaid and Medicare will probably not cover your long-term care needs for the following reasons:

- If you have built a nest egg, you will not qualify for Medicaid since, generally, you must have $2,000 or less in savings and other assets

- Medicare funding is restricted to medically necessary, acute, skilled care—such as care you would receive at a hospital or skilled nursing facility

- Benefits are generally limited to 100 days

Annual Cost of Long-Term Care

According to a 2013 cost of care study, long-term costs have continued to increase. The national average costs2, 3 involved in LTC, noted below, underscore the importance of planning.

Two Different Approaches to LTC

A traditional LTC insurance policy allows you to customize the policy’s benefits and features to emphasize what is most important to you. When choosing this option, you should carefully consider the following:

- Inflation

- Benefit period

- Deductibles or waiting periods

- Prior hospitalization requirements

- Premium increases

- Service providers

- Third-party notification

- Alzheimer’s coverage

- Spouse separate shared-care or survivor benefit rider

- Tax-free benefits that may increase over time to help offset inflation

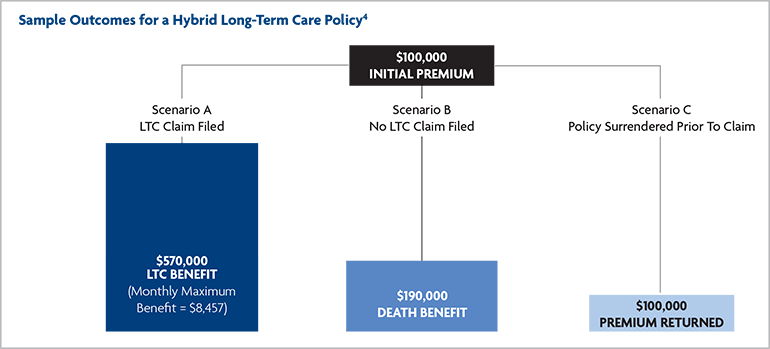

Another effective option is a hybrid LTC policy which combines LTC protection with a traditional life insurance policy. With these policies, the value of your death benefit is available to pay for covered extended health care services after the elimination period has been satisfied. Also, your policy’s benefit value could be increased up to 200% or more of the initial specified death benefit to help you meet long-term care expenses. (Scenario A, below)

This type of policy avoids the “use-it-or-lose-it” aspect of traditional LTC insurance. With specialized life insurance, if no long-term care benefit is paid prior to death, an income-tax free death benefit will be paid to the policy owner’s beneficiary upon death. (Scenario B, above)

In addition, some policies offer a return-of-premium feature that returns the original premium to the policy owner if the policy is surrendered prior to a claim being filed. (Scenario C, above)

Understanding your Choices

When purchasing LTC insurance, look for providers that have been in the LTC insurance business for 10 years or more and are A-rated by companies such as, A.M. Best, Standard & Poor’s (S&P), Moody’s Investors Service or Fitch Ratings.

Talk to your Wintrust Wealth Management Financial Advisor who can help evaluate your need for LTC insurance, and if appropriate, also help you select a policy that suits your particular needs.

1. Administration on Aging, October 2017

2. U.S. Department of Health and Human Services

3. Inflation rate based on the average annual rate during the 50 years ending December 31, 2019, using the Consumer Price Index for All Urban Consumers

4. Example: 60-year-old female, nonsmoker

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.