Data tokens on this page

Financial Solutions

Financial Solutions

Invest in the Future with Charitable Lead Trusts

A charitable lead trust can be a tax-savvy means of charitable gifting that also serves to pass wealth to future generations.

A charitable lead trust (CLT) is often thought of as the inverse of a charitable remainder trust. It is an irrevocable trust that provides a fixed amount or a percentage of the trust assets paid to a charity for a term of years or for the life of an individual or individuals. The remainder interest is either retained by the donor or given to a non-charitable beneficiary, usually a family member. A CLT is often created for lifetime giving and for estate planning purposes.

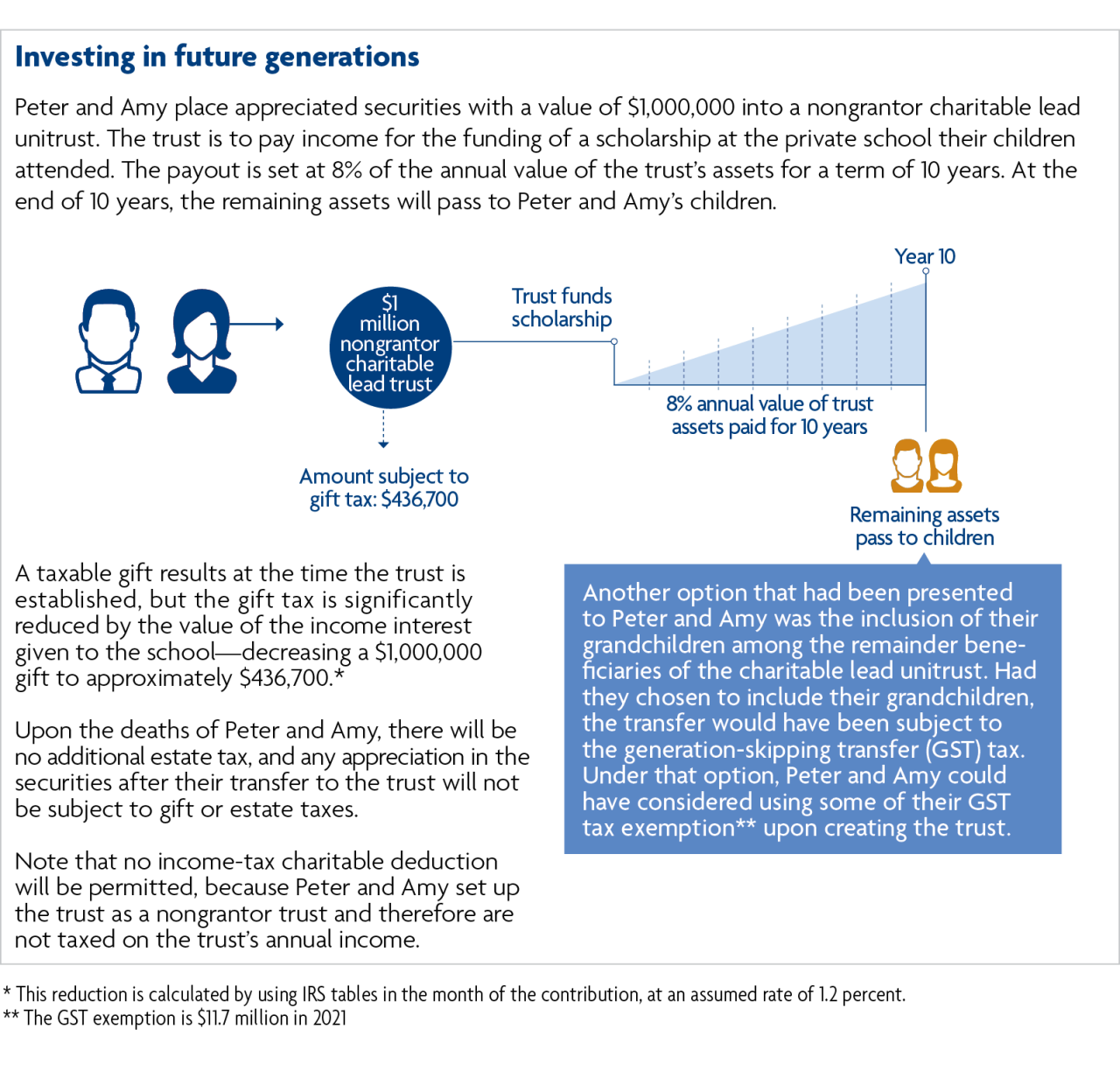

The example below illustrates how CLTs can be used to powerful effect for both charitable gifting and transferring wealth to heirs.

Generally, the income-tax benefits of a CLT may not be as significant as the estate- and gift-tax benefits. For income-tax purposes, a CLT can be structured as a grantor trust, meaning the income earned by the trust is taxable to the grantor, or a non-grantor trust, meaning the income earned by the trust is taxable to the trust.

For estate- and gift-tax purposes, there are other benefits of a CLT. If the contribution to the CLT is made during the donor’s lifetime, then the donor will also be eligible for a gift-tax deduction with the interest going to charity. If the remainder beneficiary is not the donor, then the donor could be subject to gift tax on the actuarial value of the remainder interest.

Although there can be significant tax benefits to establishing a CLT, the donor should be aware of the potential implications of the generation-skipping transfer tax. If the remainder beneficiaries are or could be the donor’s grandchildren, when a distribution from the trust is made to these beneficiaries, the distribution will be subject to this tax unless the donor or the donor’s estate is able to allocate the donor’s generation-skipping tax exemption to the transfer or bequest. This tax can be significant.

The strategy works best for wealthy donors who anticipate having a taxable estate, already have ample cash flow for daily needs, have a keen interest in lifetime charitable giving, and wish to leave an inheritance to heirs.

In summary, for investors anticipating having a taxable estate, with ample current cash flow, a desire to provide lifetime charitable giving, and who wish to leave an inheritance to heirs, a charitable lead trust offers a number of distinct benefits:

- The charity benefits by receiving a reliable stream of income for as long as the trust lasts.

- Remaining assets transferred to non-charitable beneficiaries can be transferred free of federal gift and estate tax. For example, the donor could put $1 million in a charitable lead trust and end up with several hundred thousand dollars for heirs while enjoying the same gift- and estate-tax benefit as if the donor had simply written a $1 million check to the charity.

- The donor receives a gift- or estate-tax deduction for the value of property given to the trust that is designated for charity.

- In addition, if the lead trust is structured as a “grantor” trust for income-tax purposes, the donor is permitted to take an immediate income-tax deduction for the value of charity’s interest in the trust. However, the benefit of the income-tax deduction may be diluted by two factors: First, the donor will be subject to tax on all of the trust’s income during the charitable term; second, if the donor dies or the trust otherwise loses its grantor trust status during the charitable term, then the benefit of the charitable income-tax deduction is “recaptured” at that time.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.