Data tokens on this page

Financial Solutions

Financial Solutions

Is a Roth IRA Conversion Right for You?

Converting assets to a Roth IRA allows you to lock in today’s historically low tax rates and potentially maximize the funds you will have available to spend in retirement through tax-free distributions.

Reasons to Convert to a Roth IRA

Retirement planning

- Tax diversification potential—creates tax-free income for future use and allows for more flexibility to manage taxable income in retirement

- Great for investors who anticipate that their future tax bracket will be equal to or higher than it is now

Estate planning

- No required minimum distributions (RMDs) during the owner’s lifetime—the entire Roth IRA can continue to compound tax-free

- Creates a tax-free inheritance for your heirs

- Reduces your potential estate tax liability (by reducing your gross estate), when you pay the conversion tax now

Reasons Not to Convert to a Roth IRA

- You expect to be in a lower tax bracket or living in a state without income tax1 during retirement

- There are no funds outside your IRA to pay the taxes on the conversion

- Conversion may put you in a higher tax bracket this year

- You need access to converted Roth funds within 5 years

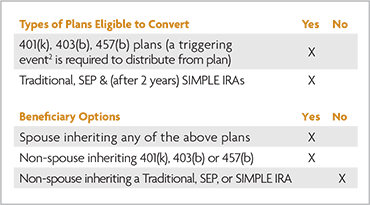

Account Types That Can Be Converted

Most retirement plans are eligible to be converted to a Roth IRA. The table below outlines the plan types and also the options beneficiaries have when inheriting retirement plan assets

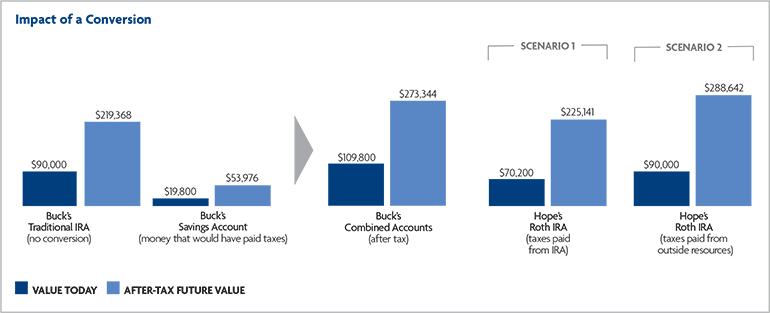

A Hypothetical Example

Hope and Buck Green, age 43 and 45 respectively, are planning to retire in 20 years. They are in the 22% tax bracket but Hope feels that it will be higher in retirement, Buck does not. Each has $90,000 in a Traditional IRA. Since Hope feels their tax bracket will increase, she is going to convert all of her money to a Roth IRA paying $19,800 in taxes. We will illustrate two scenarios for Hope showing how she will choose to pay her taxes. In scenario one she will pay the tax plus penalty from her Traditional IRA, and in scenario two, the taxes will be paid from a taxable account. Buck instead will invest the $19,800 that he would have used to pay the taxes if he executed a Roth conversion, in a taxable account.

What will the after-tax values of those accounts be like in 20 years if Hope is correct and their tax bracket increases to 24%? As you can see from the chart above, Buck’s $90,000 Traditional IRA was worth $219,368 after he paid taxes at 24%, and his savings of $19,800 was worth $53,976 after paying capital gains taxes at 15%. His two accounts are worth $273,344 after taxes. Hope’s Roth IRA where the tax and penalty were paid from the Traditional IRA has an after-tax value of $225,141 and the Roth where the taxes were paid from a taxable account has an after-tax value of $288,642. Please note, assumptions include a current tax rate of 22%, a future tax rate of 24%, and a rate of return equal to 6%.

As you can see from this hypothetical example, your tax rate, rate of return on your investments, and funds used to pay your taxes have a lot to do with how beneficial a Roth conversion will be to you.

Understanding Your Choices

Talk to a Wintrust Wealth Management Financial Advisor to learn more and determine if a Roth conversion is an appropriate retirement and/or estate planning strategy for your particular situation.

1. Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming

2. A triggering event is an event that makes a participant eligible to make withdrawals from a qualified plan, 403(b), or 457(b). Triggering events are defined in the plan document and may include: attaining retirement age, separation from service, death, disability, termination of plan by employer without replacement of another qualified plan, and in-service withdrawal for certain circumstances. (Treas Reg 1.401-1(b)(1)(ii))

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.