Data tokens on this page

Financial Solutions

Financial Solutions

A Guide to Maximizing Social Security

For over 80 years, Social Security has been a key part of how Americans ensure their financial security after they retire.

Social Security provides an unmatched combination of inflation-fighting increases, longevity protection, investment risk elimination, and spousal coverage—potentially making it one of the most valuable sources of retirement income. One out of every four households and one out of every six Americans receive these critically important benefits.

As reliable as Social Security has been, it has often gone through major changes, and 2016 was an unusually active year for the program as important legal revisions took effect. The biggest change to Social Security in 2016 was the elimination of both the so-called “file and suspend” strategy and the restricted application or “file as a spouse first” strategy.

Despite its significance—and because of its ever changing complexities—many retirees today do not understand how their Social Security benefits really work and most never focus on how to maximize the very benefits that may help sustain them throughout retirement. A recent survey conducted by Nationwide found that 38% of all retirees regret the decision they made regarding when and how to collect benefits. These can be costly mistakes as the lifetime value of a family’s benefits forgone by virtue of sub-optimal decisions can be hundreds of thousands of dollars.

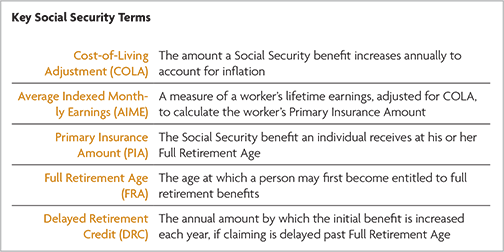

To help in the decision-making process, there are a growing number of tools and resources available. However, the rules by which Social Security benefits are distributed are complex, and there are a myriad of options available to beneficiaries. To best take advantage of these tools and make informed decisions with a financial professional, a basic understanding of Social Security is needed. The first step in that regard is to gain familiarity with some key terms. The most important of these are shown below.

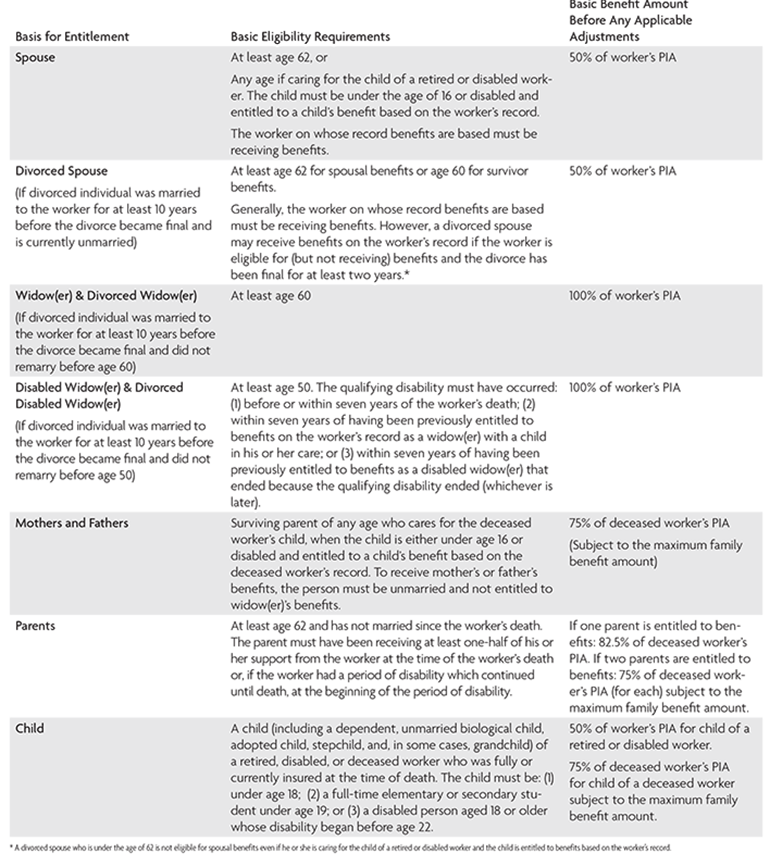

Though it is often thought of as a program that provides benefits only to retired or disabled workers, approximately 17% of current Social Security beneficiaries are the dependents and survivors of retired, disabled, or deceased workers.1 These include spouses, divorced spouses, or children of retired or disabled workers as well as widow(er)s, divorced widow(er)s, children, or parents of deceased workers.1

Generally speaking, beneficiaries can claim workers benefits, spousal or dependent benefits, or survivor benefits. As a general rule, anyone that worked more than 10 years and paid Social Security taxes for more than 10 years will be eligible for the workers benefit. When a worker files for retirement benefits, the worker’s spouse and dependent children may be eligible for a benefit based on the worker’s earnings.

In the case of spousal benefits, the spouse must be at least age 62 or have a child who is either under age 16 or who receives Social Security disability benefits in her/his care. To qualify for dependent benefits, the child must be under age 18, or a full-time elementary or secondary student under age 19, or a disabled person aged 18 or older whose disability began before age 22.

Finally, family members may be eligible for survivor benefits after an eligible worker dies. Family members who can collect benefits include a widow or widower who is: (a) 60 or older; or (b) 50 or older and disabled; or (c) any age if he or she is caring for the worker’s child who is younger than 16 or disabled and entitled to Social Security benefits the worker’s record.

Children can receive survivor benefits, too, if they are unmarried and: (a) younger than 18 years old; or (b) between 18 and 19 years old, but in an elementary or secondary school as full-time students; or (c) age 18 or older and severely disabled (the disability must have started before age 22).

Furthermore, a lump-sum death benefit of $255 is payable to a spouse who was either living with the deceased person at the time of death, or a spouse or a child who, in the month of death, is eligible for a Social Security benefit based on the deceased person’s record. The table in the Appendix provides a summary of all family members eligible for a worker’s Social Security benefits.

How Social Security Benefits Are Calculated

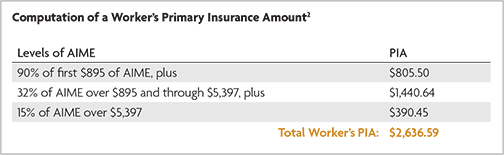

A worker’s initial monthly benefit is based on his or her 35 highest years of earnings, which are indexed to historical wage growth to determine their current averaged index monthly earnings, or AIME. If a worker has fewer than 35 years of earnings in covered employment, years of no earnings are entered as zero in the computation, resulting in a lower AIME and therefore a lower monthly benefit. The worker’s primary insurance amount, or PIA, is determined by applying a formula to the AIME as shown in the table to the right which illustrates how an AIME amount of $8,000 would translate to PIA at full retirement age in 2018.

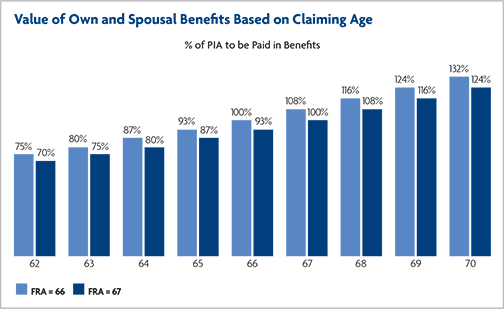

Adjustment for the Age Benefits are Claimed

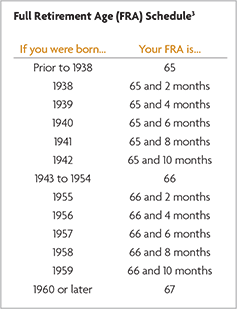

Worker and spousal Social Security benefits can be claimed as early as the age of 62; however, a worker’s initial monthly benefit will only be equal to his or her PIA if he or she begins receiving benefits at full retirement age, or FRA. A worker’s initial monthly benefit will be less than his or her PIA if he or she begins receiving benefits before the FRA. In this case, the benefit will be permanently reduced to reflect the longer expected period of benefit receipt. Specifically, a worker whose FRA is 66 and elects to claim benefits at the age of 62 would have a 25% reduction in his or her PIA. If the worker’s FRA is 67, the decision to claim benefits at the age of 62 would result in a 30% reduction in his or her PIA.

On the other hand, a worker’s initial monthly benefit will be greater than his or her PIA if he or she begins receiving benefits after the FRA. Workers who delay filing for benefits until after the FRA receive a delayed retirement credit, or DRC. The DRC applies beginning with the month the worker attains the FRA and ending with the month before he or she attains the age of 70. For workers born in 1943 or later, the DRC is 0.67% per month, which is an 8% annual increase in benefits. Workers born prior to 1943 receive a lower DRC varying from 5.5% to 7.5% annually. The chart below shows the penalties and credits associated with this timing.

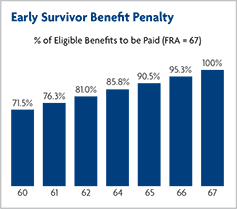

Further, survivor benefits, which can be claimed as early as age 60, are subject to reductions if claimed before FRA. The chart entitled “Early Survival Benefit Penalty” below illustrates the impact of early claims.

Clearly, the timing associated with filing a claim can have a significant effect on the lifetime value of benefits. The effect is made all the more important given the trend of increasing longevity. Today, a healthy 65-year-old female has a 50% likelihood of living until age 88 and for a couple both aged 65, there is a 50% likelihood that at least one of them will live into their early 90s.4

Maximum Benefits Limit

In 2018, the maximum Social Security benefit available to a worker retiring at FRA is $2,788 per month. However, the total amount of Social Security benefits payable to a family based on a retired or deceased worker’s record is capped by a maximum family benefit amount (MFB) based on the retired or deceased worker’s PIA.

For the family of a worker who reaches age 62 or dies in 2018 before attaining age 62, the total amount of benefits payable will be computed so that it does not exceed:

- 150% of the first $1,144 of the worker’s PIA, plus

- 272% of the worker’s PIA over $1,144 through $1,651, plus

- 134% of the worker’s PIA over $1,651 through $2,154, plus

- 175% of the worker’s PIA over $2,154.

Ultimately, this formula yields a MFB that is between 150% and 187% of the worker’s basic Social Security benefit, or PIA.5 To illustrate, consider a worker, Helen, with a PIA of $2,000. Her MFB will be $3,500, which equals $1,584 plus $1,273 plus $620 plus $23. The difference between $3,500 and $2,000 is $1,500—which is the amount of auxiliary benefits that can go to Helen’s family. Note that even if Helen claimed Social Security early, which means her benefits were lower than the value of her PIA, it would not change the $1,500 amount of auxiliary benefits. However, when Helen dies, the entire $3,500, which includes the PIA amount, becomes available in auxiliary benefits.

It is quite common for family claims to exceed the MFB cap. If this were to happen in the example above, anyone other than Helen that files a claim on her record would see their benefits proportionately reduced until the total no longer exceeded the MFB. If, for example, those claimed auxiliary benefits actually totaled $3,000, or double the allowable $1,500, all auxiliary beneficiaries would see their benefits cut in half.

However, in the event that a household has more than one worker eligible for Social Security benefits, the MFB is superseded by the combined family maximum, or CFM. This formula can substantially increase auxiliary benefits to dependents of married couples who both have work records—typically multiple children of retired or deceased beneficiaries. The children can be up to 19 years old if they are still in elementary or secondary school (and older if they are disabled and became so before age 22).

Under CFM rules, the MFBs of each earner in the household are combined and the Social Security Administration is charged with determining the situation that produces the most cumulative benefits to all auxiliary beneficiaries when claims are filed. Expanding on the earlier example, assume Helen’s spouse, George, also worked and both have PIAs of $2,000 and MFBs of $3,500. A qualifying child would still have their benefits limited by the MFB of a single parent. But the CFM used to determine the size of the family’s benefits “pool” doubles this to $7,000 a month, permitting total auxiliary benefits of up to $3,000.

However, like MFB, CFM is subject to a cap, which in 2018 is $5,322.60. Subtracting one of the $2,000 PIAs from this amount leaves Helen and George with up to $3,322.60 in auxiliary benefits for their family. So it is quite possible that three, four, or possibly more of their children would get full child benefits in this household.

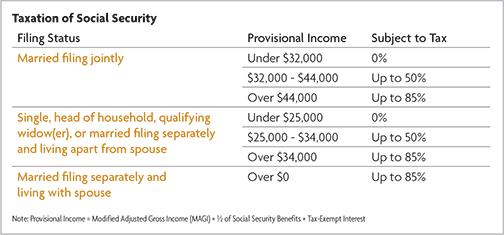

Taxation

Up to 85% of a person’s Social Security benefits can be subject to federal income tax depending on the recipient’s modified adjusted gross income (MAGI) for tax purposes and their filing status per the table below. Today, roughly half of all Social Security beneficiaries are affected by the income taxation of Social Security benefits.6

The Earnings Test

For Social Security beneficiaries claiming benefits prior to FRA and continuing to earn income, benefits are subject to a reduction. Specifically, $1 in benefits will be deducted for each $2 earned above an annual limit. In 2018, that limit is $17,040. In the year FRA is reached, benefits are reduced $1 for every $3 earned over an annual limit of $45,360 (as of 2018), until the month in which FRA is reached. Once FRA is reached, the deductions end completely. The earnings test only counts W-2 or 1099 self-employment earnings, and excludes pensions, interest, Social Security, and dividend income.

However, the apparent penalties are not what they seem. Once FRA is reached, Social Security recalculates—and increases—future benefits to account for any dollars withheld. Therefore, the earnings test should not be a disincentive to work as total lifetime benefits will be unaffected, regardless of income earned while receiving benefits. Unfortunately, many beneficiaries are not aware of this and make the mistake of working up to the annual earnings limit and then stop.

Other Adjustments to Benefits

Other adjustments to benefits may also apply, such as those related to simultaneous entitlement to more than one type of Social Security benefit. For example, a Social Security spousal benefit is reduced if the person is receiving a Social Security retired-worker benefit. Spousal benefits are also reduced if the spousal beneficiary is receiving a pension from work that was not covered by Social Security (a non-covered pension). In addition, the Social Security benefit formula is modified to reduce benefits for a worker beneficiary who has a pension from non-covered employment in federal, state, or local governments.

Claiming Strategies

The elimination of two of the most popular Social Security maximization tools in 2016 makes it crucial for investors to be aware of their estimated Social Security benefit levels—because, in many cases, those benefits will be lower than what could have been realized employing file-and-suspend and restricted application strategies.

In many cases, this will mean that a higher-earning spouse will only be able to maximize his or her benefit level by waiting until age 70 to collect. If both spouses have worked, however, a lower-earning spouse may wish to begin collecting benefits relatively early. The decision, of course, must be made taking the couple’s health and life expectancies into consideration. If both are in poor health, the higher earning spouse may wish to take benefits earlier than 70.

If there is a substantial difference between the earnings of the two spouses, however, it could make sense for a higher earning spouse to claim before 70. This is because the lower-earning spouse will receive a spousal benefit—in addition to his or her own benefit—that will increase his or her benefit so that it equals 50% of the higher earner’s benefit once the higher earning spouse files.

Early, Full, or Delayed Retirement

While tax implications can come into play, determining the best age to begin collecting benefits largely comes down to a question of longevity. While claiming Social Security benefits as soon as possible may be tempting, as explained earlier, there is a tradeoff.

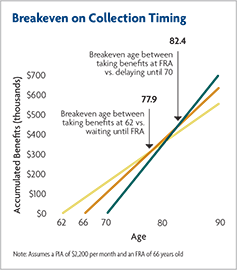

The chart to the right illustrates this tradeoff for a worker with a PIA of $2,200 per month and an FRA of 66 years old. The first breakeven example shows collecting at age 62 vs. collecting at FRA. In this example, the breakeven point is 77 years and 11 months. The second example illustrates the breakeven when beginning to collect at FRA vs. doing so at age 70 which is 82 years and 5 months.

In this case, if a worker believes they will live beyond 82 years and 5 months, they should opt to receive larger checks later and begin collection at age 70. While it is impossible to know life expectancy with certainty, reasonable expectations based on current health and family history can and should be established to inform the benefit claiming decision.

Maximize Survivor Benefits

When one member of a couple passes away, the spouse is eligible to receive their monthly Social Security payment as a survivor benefit, presuming it is higher than his or her own monthly amount. However, if the deceased began taking Social Security benefits prior to FRA, the partner’s survivor benefits are permanently limited. Many people overlook this when they decide to start collecting Social Security at age 62. If claiming is delayed until FRA, or even longer until age 70, the PIA benefit will grow and, in turn, so will the surviving spouse’s benefit after death. This strategy is most useful if the PIA of the partner in question is higher than his or her spouse’s, and if the spouse is in good health and has a longer life expectancy.

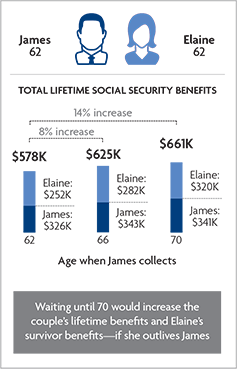

As an example, consider a couple who are both about to turn age 62. James is eligible to receive $2,000 a month from Social Security when he reaches his FRA of 66. He believes he has average longevity for a man his age, which means he expects to live to age 85. His wife, Elaine, will get $1,000 at her FRA of 66 and, based on her health and family history, anticipates living to an above-average age of 94. The couple was planning to retire at 62, and claim benefits at that time. In doing so, their monthly benefits would be 25% lower than at their FRA, meaning James would get $1,500 a month and Elaine $750 from Social Security. James also realizes taking payments at age 62 would reduce his wife’s benefits during the nine years that she is expected to outlive him.

If James waits until he is 66 to collect benefits, he would receive $2,000 a month. If he delays his claim until age 70, his benefit—and his wife’s survivor benefit—would increase another 32%, to $2,640 a month.

As shown in the graphic below, waiting until age 70 would not only boost James’ own future cumulative benefits by 5%, it would also have a dramatic impact on his wife’s benefits as her lifetime Social Security benefits would rise by about $68,000, or 27%. Even if it turns out Elaine is overly optimistic and she only lives to age 88, her lifetime benefits would still increase 12% and, together, they would collect approximately $39,000 more in Social Security benefits than if they had claimed at 62.7 In order to do this, James would either keep working or use savings to cover retirement expenses until he receives Social Security. Note that in this example, the payout figures are in 2013 dollars and before tax; the actual benefit would be adjusted for COLA and possibly subject to income tax.

Special Considerations

Lump Sum Payouts

Workers can elect to retain an option to receive a lump sum of retroactive benefits after FRA. Suppose Steven is 66 years old, has reached FRA, and decides to delay his benefit which is $2,000. He can file for his benefit and then immediately suspend it, which allows his benefit to grow via delayed retirement credits until age 70. At 69, Steven is diagnosed with a terminal illness and files for a lump sum to pay medical bills. Given that his FRA benefit was $2,000, that lump sum is worth $72,000. However, his lifetime monthly benefit will revert from $2,480 to the smaller FRA amount of $2,000—and so will the survivor benefit for Steven’s spouse.

Generally, singles who are suddenly diagnosed with a terminal illness should take the lump sum and the smaller benefit. The lump sum could go to an heir, while the monthly benefit will end at the beneficiary’s death. However, a higher-earning spouse faced with a suddenly shortened life expectancy should probably reject the lump sum. The survivor benefit will equal 100% of the higher earner’s benefit at his or her death. If the surviving spouse has a long life expectancy, the boosted survivor benefit can more than make up for the relinquished lump sum.

The Reset Feature

The reset or “do-over” feature gives some flexibility to taxpayers who may have lived to regret taking a reduced benefit at age 62 instead of their full benefit at FRA, or the bonus amount by delaying retirement to age 70. It allows a beneficiary to reset their benefit amount by essentially coming out of retirement by filing Social Security Form 521, or a “Request for Withdrawal of Application,” repaying all Social Security benefits received to date with no interest or adjustment for inflation, then reapplying at a later date to receive a larger benefit. Note that the application must be filed with 12 months of initial collection of benefits. This reset process can only be done once and it is irreversible.

Deemed Filing

An applicant that files for a spousal benefit prior to FRA is considered by the Social Security Administration to have filed for their own benefit as well. This is known as “deemed filing,” and it only applies when filing is done prior to FRA. The result of this action is that both the spousal benefit being claimed and the applicant’s own Social Security benefit will be permanently reduced. As an example, a husband who is already collecting Social Security cannot have his wife take just a spousal benefit at age 62 and then switch to a presumably larger benefit based on her earnings record in the future. If she applies for benefits before FRA, she will receive the higher of the two figures, but will be locked into that reduced benefit going forward. If the wife waits until FRA to file for benefits, she would have the option to apply for just a spousal benefit and then switch later to a payout based on her own earnings history.

Unfortunately, deemed filing is a feature of Social Security that many beneficiaries do not account for, and consequently make sub-optimal claiming decisions. The general rule to remember is that when benefits are claimed before FRA, options are limited, whereas when benefits are claimed at or after FRA, there is more flexibility—and bigger payouts.

Conclusion

Clearly, Social Security is complex and requires investors to make important decisions with significant financial implications. After the recent elimination of the two popular Social Security benefit-maximizing strategies, it has become more important than ever that investors plan to make up for potential retirement income shortfalls.

The Social Security Administration (SSA) offers an online system at socialsecurity.gov that can help investors adapt and adopt claiming strategies to maximize benefits under the new rules. By using the personal earnings information provided through establishing an online account with the SSA in conjunction with the online calculators and estimations that the system offers, investors can generate a realistic picture of the role that Social Security benefits will play in their retirement income planning—along with a roadmap toward making the most of their potential future benefits. Social Security’s online system allows users to create an account that can be accessed at any time, rather than waiting to receive a paper statement that is only sent once every five years.

The online account allows investors to access their lifetime earnings history. Assessing this is crucial because the Social Security benefit is based on the amount earned each year. If there is an error in posting annual earnings, the amount of benefits received in the future may be compromised.

The online account also provides estimated benefits that will be paid depending upon whether the investor claims benefits at 62, full retirement age, or age 70. Information on survivor and disability benefits is also contained in the online statement. Note that the estimates provide all assume a relatively consistent level of earnings in future years, but online calculators can help account for potential changes—such as a reduction in earnings if an investor cuts back on work before collecting benefits.

Although there is no perfect answer to retirement income planning, savvy Social Security benefits planning can be a key component to a healthy stream of retirement income. It is not unusual for a couple to receive around $1 million from Social Security retirement benefits over the course of their lifetime. Understanding the system and the ways to maximize benefits under it is an important consideration in retirement income planning. To learn more about the options available to you and your family, visit with a Financial Advisor at Wintrust Wealth Management.

Appendix

1. Source: SSA, Monthly Statistical Snapshot, January 2018, Table 2. See the latest edition of the Monthly Statistical Snapshot at http://www.socialsecurity.gov/policy/docs/quickfacts/stat_snapshot/index.html.

2. Source: SSA

3. Source: SSA, 2013 Social Security/SSI/Medicare Information, February 28, 2013, available at http://www.socialsecurity.gov/legislation/2013factsheet.pdf.

4. Source: Annuity 2000 Mortality table, Society of Actuaries

5. Benefits for a divorced beneficiary are not taken into account for purposes of the family maximum. SSA, Program Operations Manual System (POMS), Section RS 00615.682, “Family Benefits Where a Divorced Spouse or a Surviving Divorced Spouse is Entitled,” available at https://secure.ssa.gov/apps10/poms.nsf/lnx/0300615682.

6. Source: Congressional Budget Office

7. All lifetime benefits are expressed in present values, calculated using an inflation-adjusted discount rate and life expectancies of 86 and 88 for husband and wife respectively. The numbers are sensitive to, and would change with, the discount rate and life expectancy assumptions.

8. Source: Congressional Research Service. Table shows the minimum eligibility age for each type of benefit (i.e., the age at which benefits are first payable on a reduced basis). The maximum family benefit may apply, reducing the benefit received by each family member on a proportional basis. The maximum family benefit varies from 150% to 188% of a retired or deceased worker’s PIA. For the family of a worker who is entitled to disability benefits, the maximum family benefit is the lesser of 85% of the worker’s AIME or 150% of the worker’s PIA, but no less than 100% of the worker’s PIA. Other benefit adjustments may apply.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.