Data tokens on this page

Financial Solutions

Financial Solutions

Capture Ratios

Managing portfolios in today’s volatile environment.

Jeffrey G. Sweno, MBA

Senior Vice President

Wintrust Investments

The world of investing has changed dramatically over the past decade. As the market turmoil of the 2008 financial crisis revealed, simply having a well-diversified portfolio no longer provides the capital protection that investors had come to expect based on prior experience. Accordingly, advisors and investors have sought more sophisticated ways to screen investments. Two concepts that have recently been gaining broad acceptance are the up-capture and down-capture ratios.

Generally speaking, these ratios differentiate investment performance during bull and bear markets. Up-capture compares an investment’s performance against its benchmark during periods when the benchmark’s performance is positive, while down-capture compares the investment’s performance against its benchmark during periods when the benchmark’s performance is negative. If a mutual fund has an up-capture of 100 or higher, then the fund will have a return equal to or greater than its benchmark. Correspondingly, if the downside capture ratio is less than 100, then the investment’s loss will be less than that of its benchmark in a down market. In today’s investing landscape, capture ratio analysis should be used as a starting point when looking to build portfolios that are truly aligned with an investor’s tolerance for risk and loss.

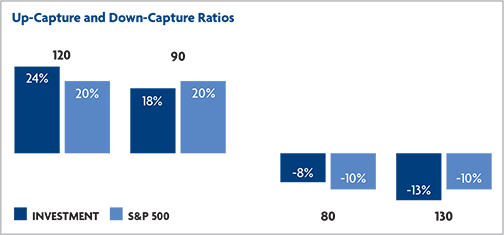

For example, if the average upside return over a given period of time for the S&P 500 was 20% and the return on a particular investment benchmarked to the S&P 500 was 24%, then the upside capture would be 120. Conversely, if the average downside return on the S&P 500 was -10% and the same investment had an average return during that period of -8%, the downside capture ratio would be 80 (see graphic below).

For most investors, the primary goal is to build a capital base that will sustain them through retirement. To that end, the old adage, “it is not what you make, but rather what you keep,” is worth bearing in mind. When an investment falls 50%, it does not recoup that loss with a subsequent 50% rise. To illustrate, on March 9, 2009, the S&P 500 closed nearly 57% below its peak value notched less than 18 months prior. It did not return to that peak level until a 131% run-up which took over four years to complete.

One of the most effective ways to minimize losses while building a capital base is to use capture ratios to find investments that achieve good returns during market run-ups without participating as much in the downside during negative market periods. Consider a portfolio benchmarked to the S&P 500 that has a down-capture ratio of 80 and an up-capture ratio of 90. During the time period noted above, this portfolio would have been off just 34% from its peak when the S&P 500 bottomed out in 2009. Moreover it would have recouped its losses in less than five months and by the time the benchmark S&P 500 had finally returned to its peak in March of 2013, the portfolio would have more than doubled.

At Wintrust Wealth Management, we believe that investors should resist the urge to focus solely on the highest return and focus more on capture ratio to achieve their investment goals. Doing so is one step towards adopting more robust investment selection processes to compliment the basic benefits of diversification. To learn more about capture ratios and ways to improve how you build your capital base for the long-run, contact one of our professionals.

Request an Appointment

Ready to start a conversation?

Call us at 847-482-8480 or:

Serving Clients At:

Jeffrey G. Sweno, MBA also serves clients by appointment at the following locations: