Data tokens on this page

Financial Solutions

Financial Solutions

The Asset Allocation Investment Process

Over the years, financial experts have provided investors with different theories and ideas on how to invest effectively. The one concept that almost everyone seems to agree upon is the need to diversity.

Although the stock market has historically trended up over time, making it an attractive investment vehicle for the long-term investor, bear markets and corrections are a reality. An ill-timed market dip can knock an aggressively allocated retirement portfolio off track.

The challenge, of course, is trying to determine when one cycle will end and another will begin. Thankfully, that is not necessary and, as it turns out, timing the market rarely works.

Understanding Asset Allocation

The practice known as asset allocation is the most effective method for most investors to balance a portfolio among various types of investments and shield it against offsetting losses. As many investors realize, the three main asset classes—stocks, bonds, and cash alternatives—are often co-classified (in the same descending order) as higher-risk, lower-risk, and lowest-risk investments. Within each asset class, investment risk can be further broken down. For instance, a large cap stock from a major corporation with a track record of stability is usually considered a lower-risk investment than a stock issued by a lesser-known company with a smaller market capitalization. On the other hand, the small cap stock generally carries the potential for higher returns.

Developing Your Strategy

After deciding that asset allocation makes sense, the primary objective is to decide how to diversify your portfolio. For this task, and for the ongoing maintenance it will require, your Financial Advisor is an invaluable resource. At Wintrust Wealth Management, we can help you develop an asset allocation strategy that is aligned with your investment objectives and risk tolerance. To make the process simpler, we have developed investment strategy models that cover a wide spectrum of asset allocations and serve as a guide to asset class breakdowns for various investment styles. For instance, investors seeking growth and income with a moderate risk tolerance would want approximately half of their portfolio invested in stocks, a third in traditional fixed income investments, and the remainder in alternative income investments with a marginal amount in cash alternatives. A growth-oriented, long-term investor, on the other hand, would be almost entirely invested in stocks.

Diversification as a theoretical concept is easy to understand but until the last 20 years has been difficult to implement. Most of us recognize the need to diversify our investments among stocks, bonds, and cash alternatives. But how do you determine what percentages to allocate among them? In the 1950s a concept was developed called “modern portfolio theory” to address this very concept.

Two Major Tenets of Modern Portfolio Theory

1. Investors are risk averse. That means given the choice between investments with the same general returns, they will choose the least risky.

2. The more risk an investment has, the greater the return potential should be. Because investors are risk averse, they will not choose investments with greater risk without the possibility of greater return.

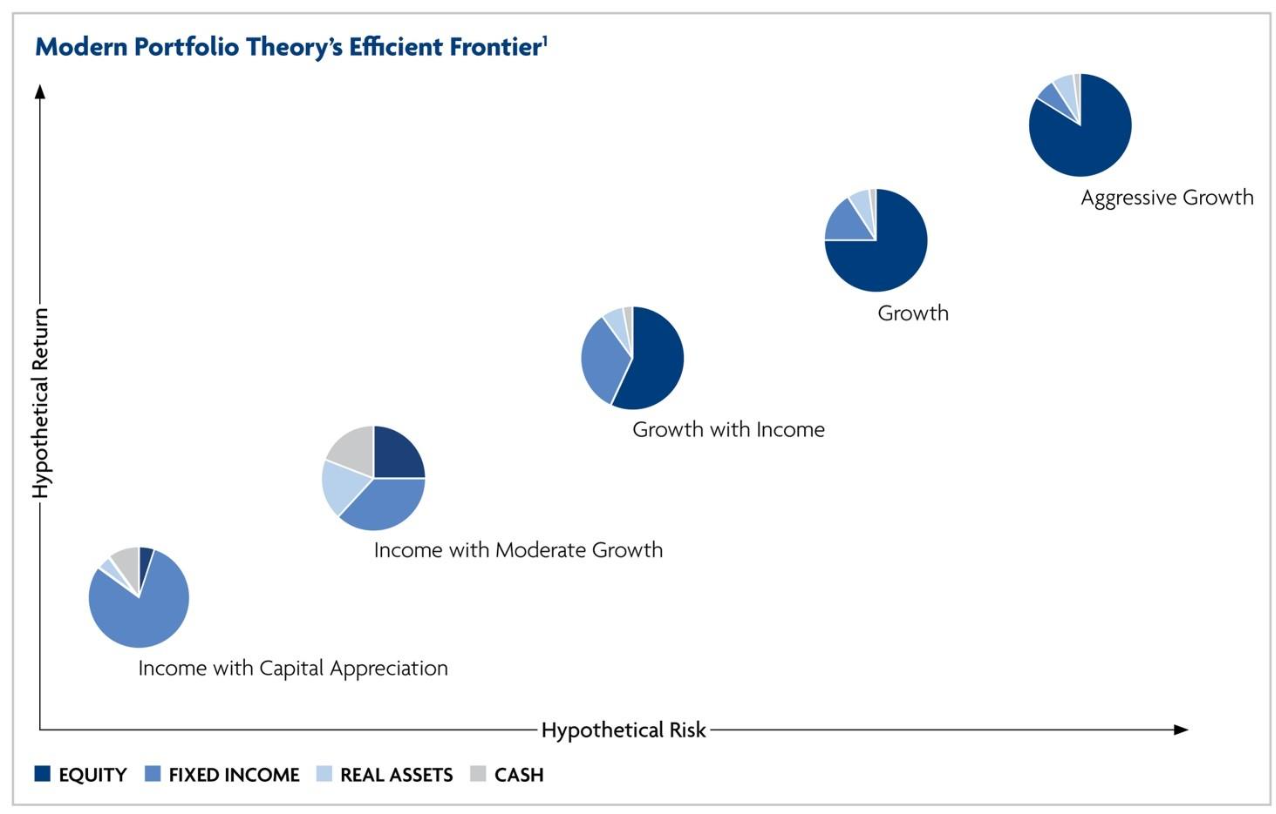

Financial Advisors use these tenets in the development of portfolios for investors. Our asset allocation models are indicated in the chart below. Moving left to right, the chart shows allocation recommendations with higher levels of portfolio risk and correspondingly higher levels of expected return.

Investors with similar investment objectives may have different risk tolerances, therefore these asset allocation models provide recommendations for investors with different degrees of risk tolerance.

What Kind of Investor Are You?

Using the investment planning process WealthVisionSM our financial advisors can determine which investment objective is right for you from among the many shown on the chart below.

Income with Capital Appreciation

These investors seek the maximum amount of income consistent with a modest degree of risk. They are willing to accept a lower level of income in exchange for lower risk. Higher risk investments, such as high yield bonds and some equities, are typically not a large percentage of the account.

Income with Moderate Growth

These investors seek the maximum growth and income consistent with a relatively modest degree of risk. They are willing to accept lower potential returns in exchange for lower risk. Equities, generally dividend paying equities, may be some percentage of the account.

Growth with Income

These investors seek to balance the risk of capital loss with higher potential growth and income. High yield bonds and equities, generally dividend paying equities, may be a significant percentage of the account.

Growth

Growth investors seek a significant level of growth and income, are financially able and willing to risk losing a substantial portion of investment capital, and due to their long term horizon or other factors they pursue high risk, more aggressive strategies that may offer higher potential returns. High yield bonds and equities, generally dividend paying equities, may be the primary assets in the account.

Aggressive Growth

Aggressive Growth investors seek a significant level of growth, are financially able and willing to risk losing a substantial portion of investment capital, and due to their long term time horizon or other factors, they employ higher risk, more aggressive strategies that may offer higher potential returns. Higher risk investments such as equities may be as much as 100% of the account.

Asset Allocation Over Time

It is important to realize that asset allocation can shift over time due to varied performance of different asset classes. Also, as your personal circumstances change, you may want to reconsider your investment objective and risk tolerance. To learn more and review your current asset allocation, contact a Wintrust Wealth Management financial advisor today.

Our professionals can help you construct a strategy customized for your unique needs and best positioned to help you achieve your long-term goals.

1. Asset allocation weights are approximate and may shift over time.

Past performance is not a guarantee of future results. Diversification does not guarantee a profit or protect against loss.

Start the Conversation

Where will your financial journey take you? A Financial Advisor helps you navigate the terrain, avoid pitfalls, and keep you on track to achieve your financial goals.